A quick Autowealth Review a year on.

Basics

- Simple strategy of asset allocation and rebalancing

- Min $3,000 to start

- Fees at 0.5% + USD$18 per year

Why did I choose AutoWealth?

When I started out last year, I knew I wanted to diversified my portfolio to include more global equities, as my portfolio was very Singapore equity focused.

And also I was conscious of how the market seems to be at an all time high back in 2019, so I didn’t want to do a lump sum. I was searching for a dollar cost averaging strategy.

And lastly, I didn’t want to buy individual stocks, so I was looking for index ETFs for diversification.

I went with AutoWealth simply because of it’s simple strategy of asset allocation and rebalancing. And frankly it was the only one that I understood.

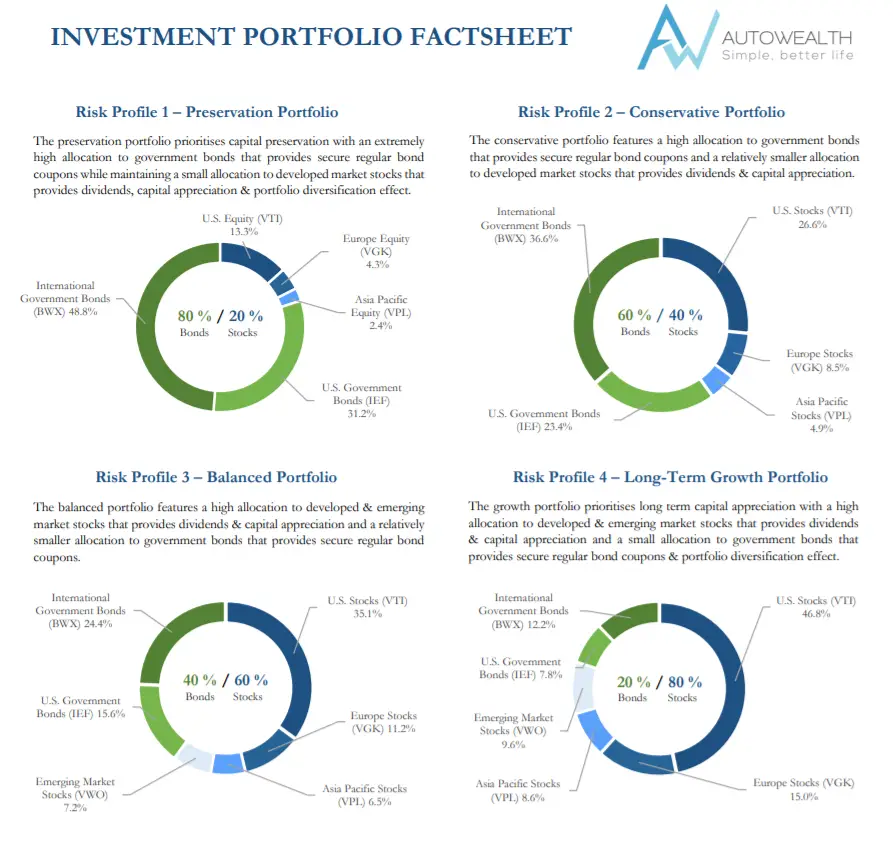

Offers 4 types of portfolio (From AutoWealth site)

From the above charts, you can tell that the portfolios are made up of these ETFs:

- Vanguard Total Stock Market ETF (VTI)

- Vanguard FTSE Europe ETF (VGK)

- Vanguard FTSE Pacific ETF (VPL)

- Vanguard FTSE Emerging Markets ETF (VWO)

- iShares 7-10 Year Treasury Bond ETF (IEF)

- SPDR® Bloomberg Barclays International Treasury Bond ETF (BWX)

The only difference is VWO is excluded from the Preservation and Conservative Portfolios.

Personally, I went with the Long Term Growth Portfolio, which suits the timeline I had.

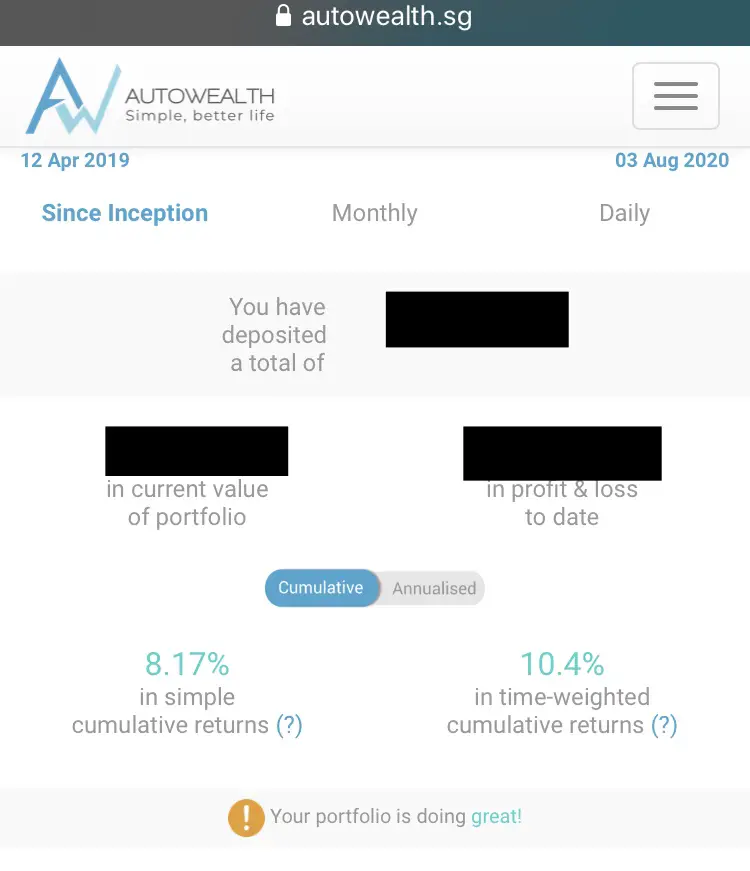

How did my Autowealth portfolio perform?

My pot is up 10% as of 3 Aug 2020. Remember, I started investing last year 2019, when market was considered to be all time high at that period.

During the march sell-off, I double my contribution amount. So that helped with the performance too.

Features

What I liked

- Flexibility

- I can increase or decrease my contribution at any time, and it takes into effect right away.

- I can even transfer over a lump sum, and the trade will be executed the next day. Unlike with the traditional RSP, trade will only be executed on a certain date.

- Auto rebalancing duh!.

Minor irks

- One thing to note, Autowealth doesn’t allow fractional shares. With a smaller amount contribution, there are trades where it would just buy into 2 or 3 of the ETFs instead of all 5. However, when I doubled my amount, then I do see that it is able to buy into almost all the ETFs. So I think if you are considering using dollar cost averaging strategy, make sure your monthly contribution amount is of considerable amount.

Other than that, I really like what Autowealth has done so far. And honestly, it beat my DIY Singapore portfolio too. Maybe it’s time to reconsider my DYI portfolio.

Summary

Automating my investment is my favorite way of investing. It takes the emotion out of investing. I have tried saving up a lump sum and trying to execute a trade every quarter. That didn’t work very well cause I always thought, it’s too pricey, or it would sell down even more. Eventually, I did nothing.

Autowealth is great tool for passive investments. As is all other robo advisor. But it is one that I understood, a simple strategy of asset allocation and rebalancing. 0.5% + USD18 is a small fee to pay, instead of opportunity cost of not being able to execute your trades due to emotions.

Check out my latest Autowealth Review: 2 Years On.

– fees of USD 18/ annum irks me because this can get increased

– no fractional shares?

– Investing 15% in VGK (Europe) in the long term portfolio? Huge drag- europe never rises- its a dead continent in terms of investment. 10 years return is 5.7%