With all the 3 local banks slashing interest rate, it is no surprise that many (including me) are turning to other alternatives to earn more interest. This is a quick review of Singtel EasyEarn (accurate as of 17/07/2020).

What is the Singtel Dash EasyEarn?

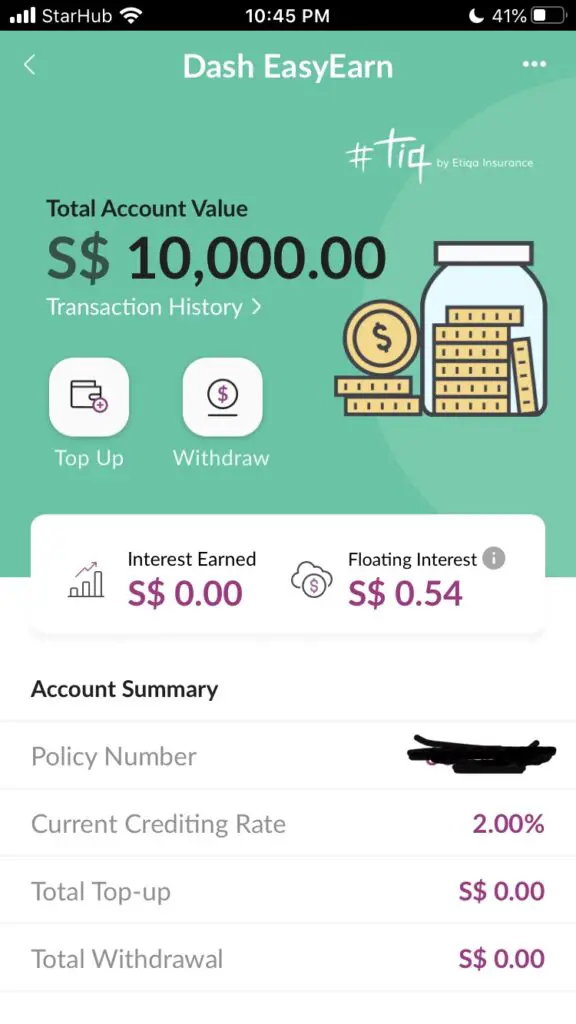

It is an insurance savings plan that pays 2% interest for the first year, with the flexibilty of topping up, and withdrawals with no lock in period or penalty.

As of 25 Sep 2020, interest rate for the first year has been reduced to 1.8% for new signups.

Why Singtel EasyEarn?

I have been using the OCBC 360 account to earn a higher interest. But with the latest cuts, my interest with Salary crediting (0.6%) + Save (0.2%) + Base interest (0.05%) works out to be only 0.85%.

As I have idle cash sitting around in my bank account, I’m always on the lookout for ways to earn higher interest. Singtel EasyEarn sounds like a no brainer to me, with a 2% interest on the 1st year.

Signup Process

As I already had a Singtel Dash account, all I had to do was login to the app, click on the Grow Money icon, and follow the steps. Payment can only be done via eNets. It was relatively seamless, and I was done in 10 mins.

What is the catch?

This was the exact same question that I was asking when I first heard about the Singtel Dash EasyEarn. This is after all a single premium life insurance plan.

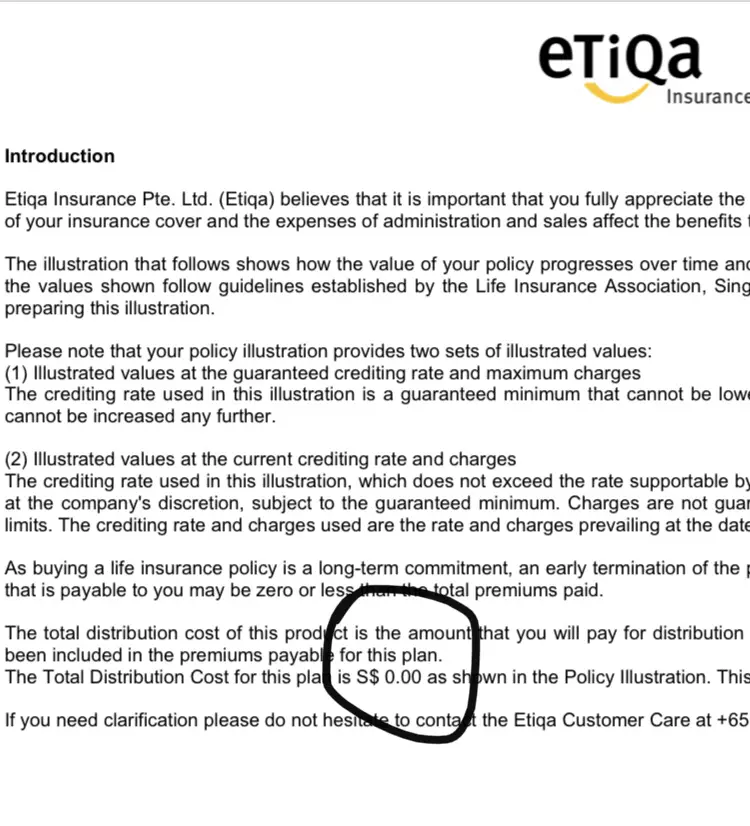

I can confirm that there are No Fees associated with this plan, as per the policy document.

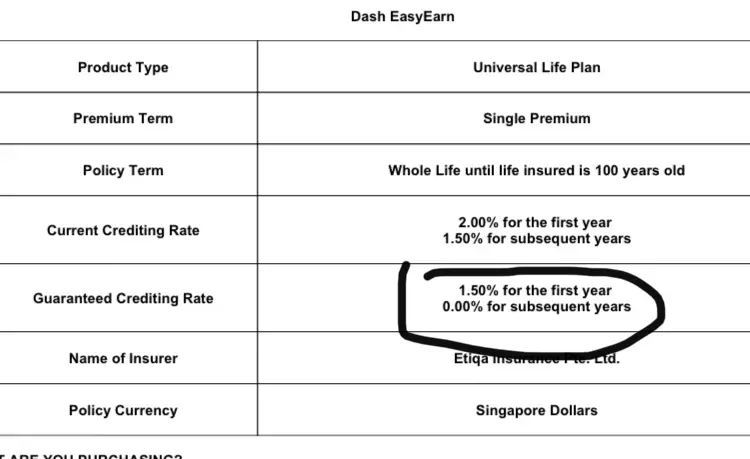

There is however a tiny catch. Remember I was saying that this plan earns a 2% interest for the 1st year. This brings me to the Guaranteed Crediting Rate.

Guaranteed Crediting Rate

Put simply, a Guaranteed Crediting Rate refers to the guaranteed rate of interest for a specific or fixed period.

In this case, with the Singtel Dash EasyEarn, the guaranted interest rate is 1.5% for the 1st year and 0% for the subsequent years.

This means that the provider, in this case eTiQa may revise the interest rate down to a min of 0% after 1st year.

Like I mentioned, this is a tiny catch, which may or may not happen. Just like the interest rates in bank saving accounts, there is no guaranteed of a fixed interest rate.

Summary

Pros

- 2% interest rate for the 1st year

- 100% capital guaranteed

- No lock in periods – you can withdraw out anytime

- Min deposit $2,000

Cons

- Non guaranteed interest rate after 1st year

- Deposit is capped at $20,000

- Transaction fee of $0.70 per partial withdrawal request. Free if withdrawal is into Dash Wallet

I am always on the hunt for higher interest rates for my idling cash. I would say go for it if you have cash in your low interest rate account. You get 2% interest rate for the first year. E.g you put $20,000, you will earn $400 in the 1st year. No min salary credits or any criteria to hit in order to earn the 2%. Why not?

Even though the interest rate isn’t guaranteed after the 1st year, you could always withdraw it after the 1st year with no penalty. Win-win for us ?