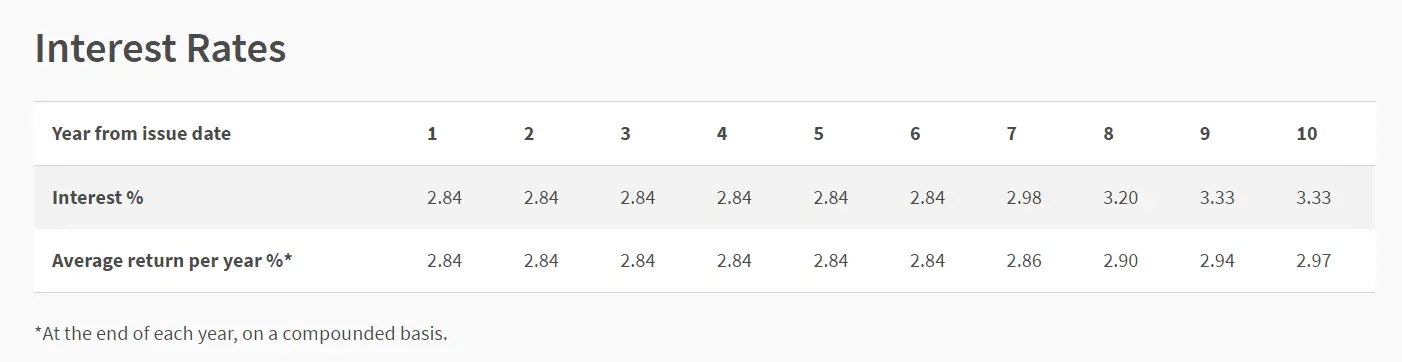

The interest rate for Singapore Savings Bond (SSB) Feb 2023 (SBFEB23 GX23020X) is at 2.97% p.a. if held to maturity.

If you invest $10,000, and hold it to Maturity at the 10th year, you would have earned $2,988.

The 1st year’s interest rate is at 2.84%. If you decide to redeem after the 1st year, you will still earn $284.

Why is interest rate high?

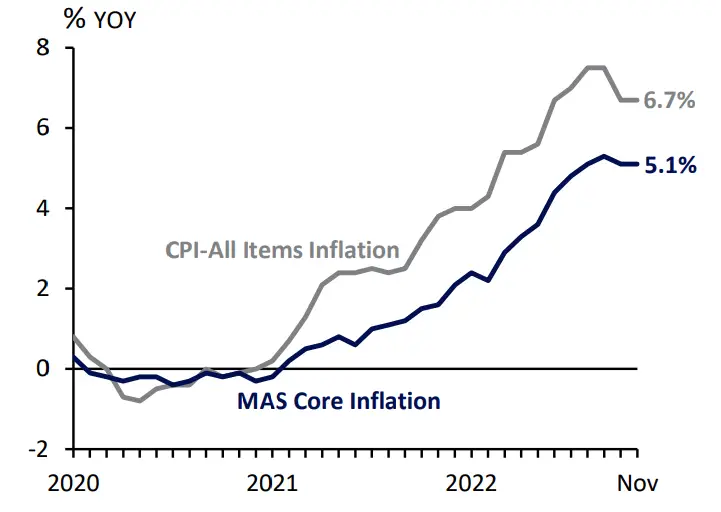

Simple answer is because inflation is rising. Although the core inflation rate for Singapore has remain flat at 5.1% in Nov, it is still well above the 2% inflation target.

Inflation usually means that there is more demand than supply, thus causing prices to increase.

By increasing interest rates, this makes borrowing more expensive. So lesser people will borrow money to buy things. And hopefully this will bring the demand down, and when there is less demand, then inflation will fall.

From the graph above, we can see that the inflation seems to be falling from the previous highs.

How are SSB interest rates determined?

The SSB on offer in any given month are linked to the daily average SGS yields as published by MAS

in the previous monthhttps://www.mas.gov.sg/-/media/MAS/News-and-Publications/Press-Releases/Annex-1-FAQ.pdf

Please check out this post for a detailed guide on predicting the future SSB rates.

Should you buy?

It depends on how long do you plan to hold these bonds?

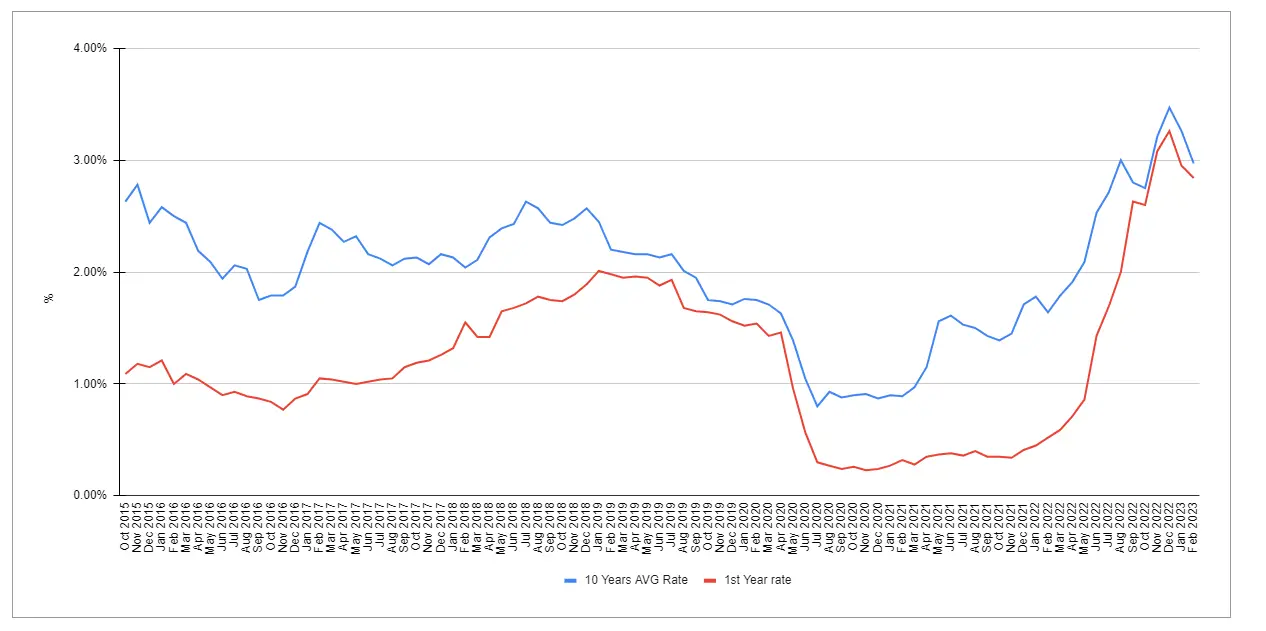

If you are looking to lock in rates for the next 10 years, SSB can be considered. Because since 2015 (when SSB was introduced), we have never seen rates rise above 2%, until mid of 2022.

But if you are just looking to get more interest on your money for the next 6 – 18 months, perhaps you should consider Fixed Deposits. They have much better rates now compared to a couple months ago. One can also consider applying for T-bills instead.

And also, if you are able to hit the different criteria to qualify for the higher interest rates in the OCBC 360 (up to 7.65%), DBS Multiplier (up to 4.1%) or UOB One Account (up to 7.8%), then you should leave your money in the bank to earn those interest instead.

I’ve seen the hype recently that people are bidding on T-bills and buying up SSBs and Fixed Deposits. It is always good to have a portion of money in these safe assets. But don’t forget that, ultimately, 3-4% of interest is not going to beat the inflation rate we are experiencing now.

Depending on your risk appetite, it might also be a good time to consider allocating some cash into some broad based market funds such as S&P500 index fund or a MSCI world index fund.

Comparison between SSB and other similar products.

OCBC Time Deposit

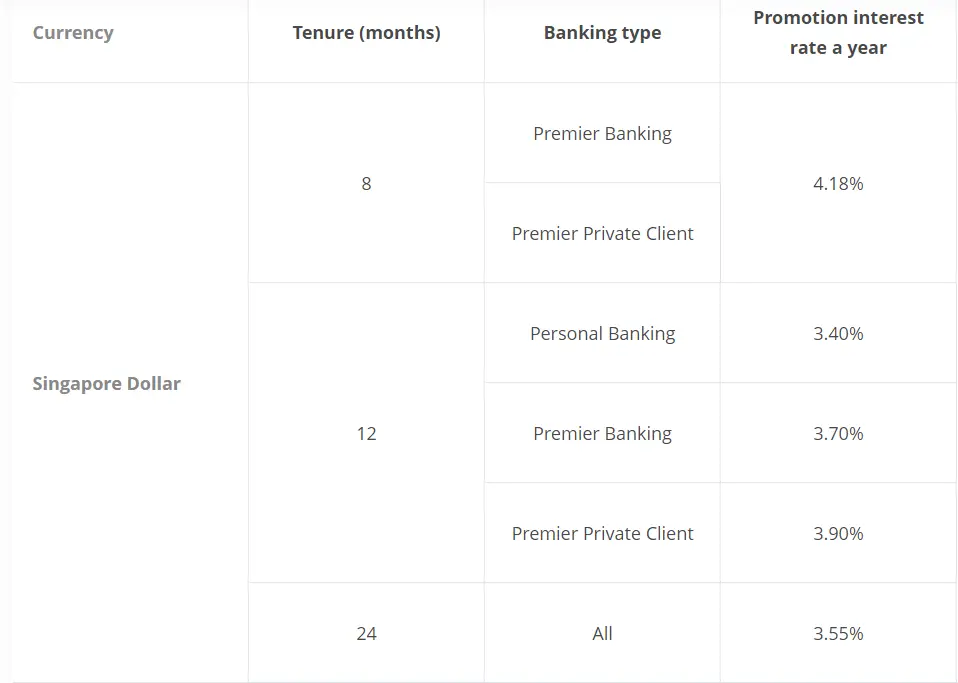

At the moment, OCBC is running some promotional interest rate between 8-24 months tenure at 3.40% – 3.90%. The one worth mentioning is the CNY promotion rates of 4.08% for 360 customers.

The down side is that your funds will need to be locked for the tenor in order to receive the interest and min deposit is $20,000.

UOB Fixed Deposit

Similarly, UOB is also running some promotional interest rates. It seems to be the highest among the banks at the moment, between 3.55% – 3.95 depending on the deposit amount.

The down side is that your funds will need to be locked for the tenor in order to receive the interest and is min deposit is $10,000.

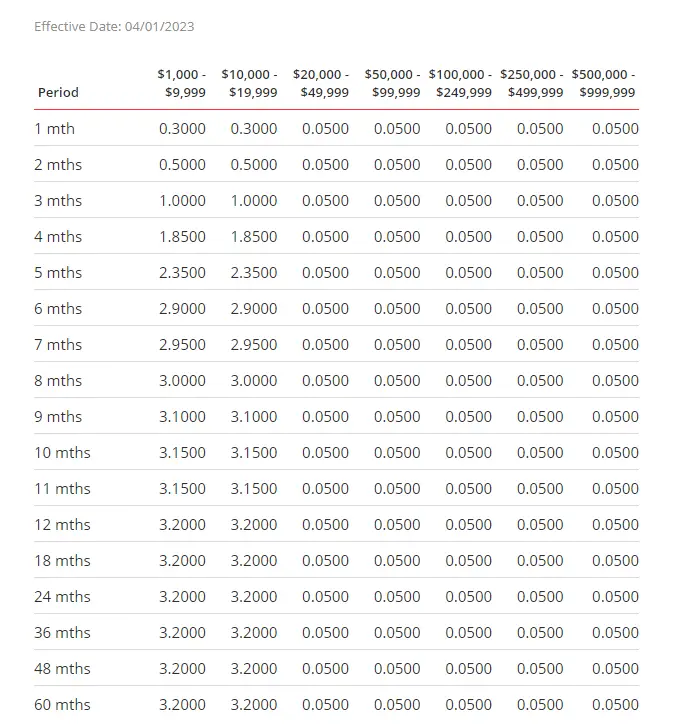

DBS Fixed Deposit

DBS has finally decided to raise it’s FD interest rates. It is between 0.3% to 3.2% depending on the Tenor and the amount. But it is still nothing comparable to OCBC’s and UOB’s or SSB.

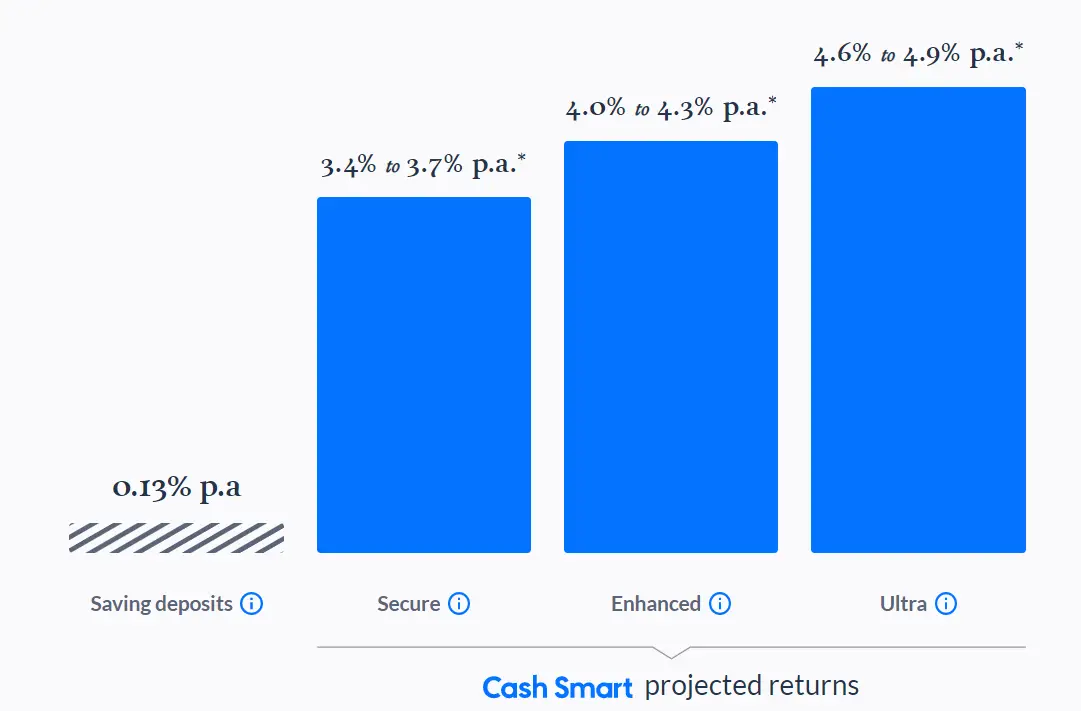

Endowus Cash Smart

Endowus Cash Smart is offering between 3.4% to 4.9% of projected returns depending on the portfolio. These are not guaranteed returns.

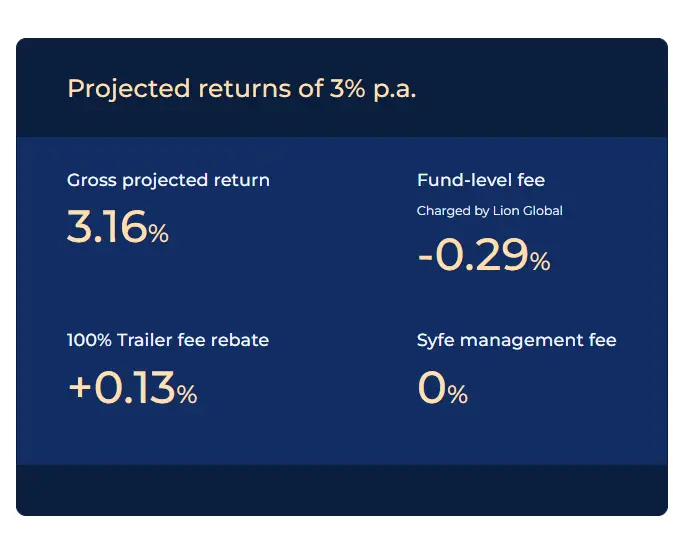

Syfe Cash +

Syfe Cash+ is offering 3% of projected returns. Again returns are not guaranteed.

Summary

| Product | Yield |

|---|---|

| SSB | 2.97% (10 yrs Guaranteed), 2.84% (1st yr, Guaranteed) |

| OCBC Time Deposit | 3.40% – 3.90% (Guaranteed) depending on on your account type, tenor and min deposit is $20,000 |

| UOB Fixed Deposit | 3.55% – 3.95% (Guaranteed) depending on the deposit amount and min deposit is $10,000 |

| DBS Fixed Deposit | 0.3% –3.2% (Guaranteed) depending on the deposit amount and Tenor |

| Endowus Cash Smart | 3.4% to 4.9% depending on the portfolio (Projected Returns) |

| Syfe Cash+ | 3% (Projected Returns) |

Based on the comparison above, one can consider SSB as it has a guaranteed 2.97% p.a and first year’s interest is at 2.84%, only if you are planning to lock in the rates for a longer period.

Otherwise, Fixed Deposit from OCBC and UOB are much more attractive, if you are considering to hold for short term period. Only downside is that the funds need to be locked for the tenure and you will need to deposit at least $10,000 or $20,000 to qualify for the rates.

Is SSB safe?

SSB is fully backed by the Singapore Government. This means that you can always get your full investment amount with no capital loss.

Singapore bonds has a credit rating of AAA. This shows that Singapore bonds has strong creditworthiness, with a very low probability rate of default.

So I think a better question is, do you trust the Singapore Government?

How to buy SSB?

You can apply through internet banking or through DBS/POSB, OCBC and UOB ATMs. Check out this Step By Step guide on How to buy SSB.

You have between now till 26 Jan 2023, 9pm to apply.

There is a min amount of $500, and in multiples of $500. And the total amount of SSB you hold cannot exceed $200,000 at any given one time .

You can find out more about this month’s SSB here.

How to check your SSB Allocation?

New SSB will be allocated on the 3rd last business day of the month (called the Allotment Day). You can check the results of your allocation after 3pm on Allotment Day.

Simply login to https://eservices.mas.gov.sg/ssb/ with your Singpass App. And you can see the results.

Can SSB be redeemed early?

Yes, SSB can be redeemed at any given month with no penalty. You will be paid the principal plus any accrued interest (prorated interest). You should redeem the bonds before the Closing Date for it to be paid out on the 2nd business day of next month.

SSB is flexible in a way that you can get your principal by next month, but it is not flexible enough if you need the money now. So you should always have a stash of emergency money in the bank before putting any into SSB.

Cash investment for SSB can be redeemed via DBS/POSB, OCBC and UOB’s internet banking or ATMs.